Italiano

Polystyrene

FOB

Producer :

China

Container Shipping Method:

Ocean transportation

Introduzione del prodotto:

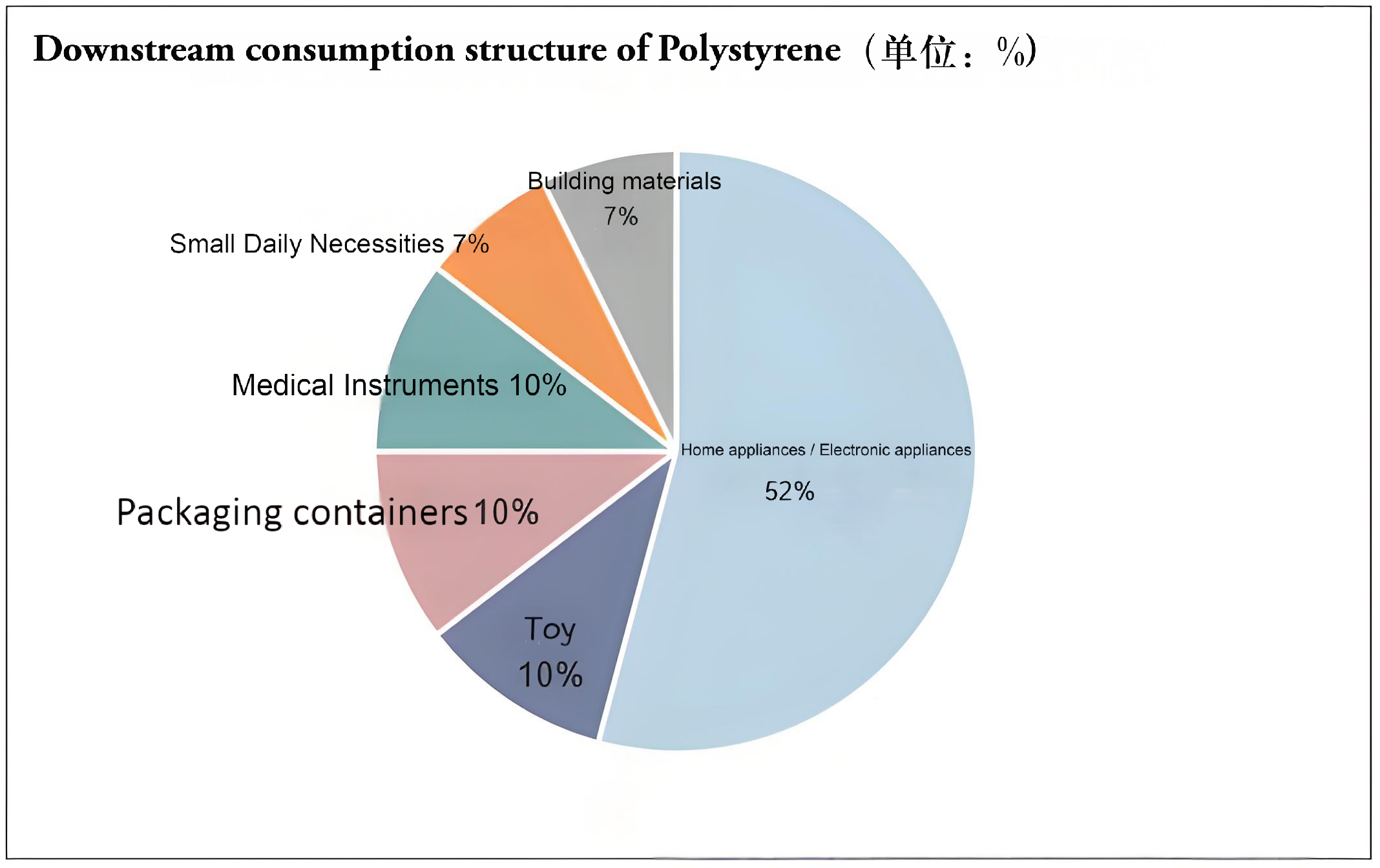

Polystyrene: The Extreme Contrast of Supply and Demand

H1 2025 saw Jiangsu Saibaolong Phase III go into operation, adding 360,000 tons of new capacity, totaling 7.28 million tons industry-wide, leading to oversupply. Output reached 2.363 million tons (+13.8% YoY), driven by new capacity release and high-load production of major plants, while downstream demand remained weak. Inventory was low in Jan; since Mar, depleted demand and US tariff hikes hindered exports, pushing inventory to 100,000 tons in Jun (+25.5% YoY) and extending the digestion cycle.

Specifiche:

Lascia le tue informazioni e

ti contatteremo.

ti contatteremo.

Upwardintl International LimtedGaoxing Car Materials Supply Chain (Guangzhou) Co., Ltd.

Dongguan Ruiqiang Plastic Import and Export Co., Ltd.

Upwardintl International Limted

Gaoxing Car Materials Supply Chain (Guangzhou) Co., Ltd.

Dongguan Ruiqiang Plastic Import and Export Co., Ltd.

: +852-2739 0068

Fax : +852-3014 5609

Mail : admin@upstar-etc.net

: www.upstar-etc.net

: Unità G, 21/F., Cos Centre, 56 Tsun Yip Street, Kwun Tong, Kln Hong Kong

HOME

HOME